Unleash the powerful value of your assets to grow your working capital

Part 3 in the Cash Cycle series: Don’t sacrifice your goals. Grow your working capital and regain control of your cash flow with asset-based lending.

Now more than ever, businesses are realizing the impact their cash flow has on their market resilience and longevity. According to one study, 82% of business failures are due to cash flow problems..

If your company is spending more money than it’s currently bringing in, you likely have a cash flow problem. This is a common issue for the majority of businesses and can signal that immediate changes are needed.

Asset-based lending to the rescue!

There can be many reasons why a business finds themselves experiencing cash flow problems and not all of them are negative. Unexpected growth opportunities are one such instance that you may find the need for extra working capital. The orders are coming in but you need cash to purchase inventory and supplies.

Turning to traditional funding options, like banks, is not always possible. You may have maxed out your current borrowing capacity or, depending on your situation, it could be difficult to secure funding from traditional sources, as the loan criteria for banks can be more rigid.

On the other hand, with options such as asset-based lending, companies that have well-established financial reporting systems can unlock working capital to keep their business thriving.

Need a quick refresher on the CCC and how to calculate it? Keep reading to review the basics of your CCC (or read more about it in part 1 of this series). Ready to learn about ABL? Skip ahead for the top 3 benefits of this powerful alternative lending solution.

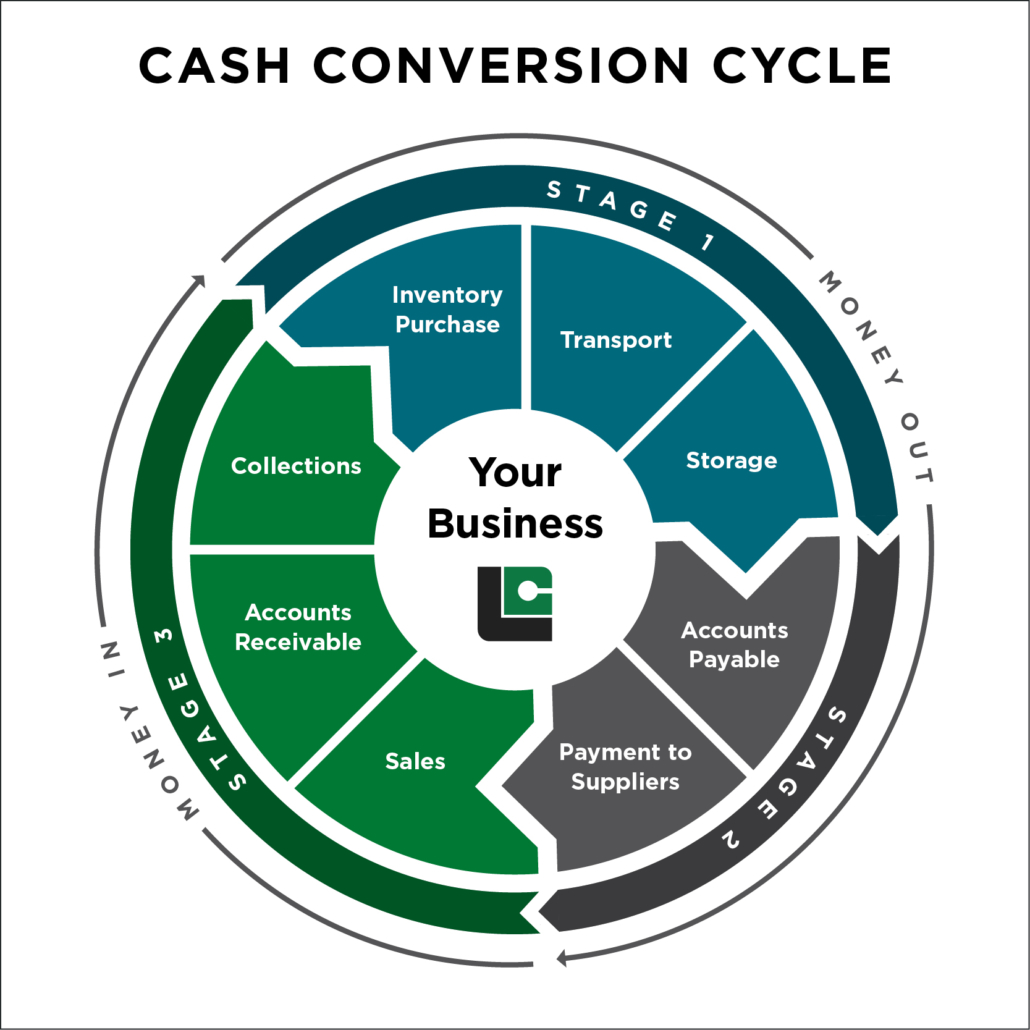

Quick Recap: What is the cash cycle?

The cash conversion cycle (CCC) tells you how many days it takes for your company to turn your inventory purchases into cash – a strong indicator of your company’s cash flow. Your CCC also helps lenders and other financial providers assess your potential risk level.

Through a fairly simple formula, you can calculate your own company’s cash cycle. The CCC is equal to the number of days it takes to sell your inventory, plus the number of days you need to collect on your sales, minus the days it takes you to pay your vendors.

| DIO | Days Inventory Outstanding | The average number of days it takes your company to turn inventory into sales. A lower number is better. |

| DPO | Days Payable Outstanding | The number of days it takes you to pay your accounts payable. The higher this number, the longer you can hold onto cash. A longer DPO (higher number) is better. |

| DSO | Days Sales Outstanding | The number of days you’ll need to collect on sales of that inventory after the sale has been made. A lower number is better. |

Want to learn more about smart cash flow strategies? Check out our Ultimate Cash Cycle Guide

ABL Advantage 1: Option-rich financing alternative

Asset-based lending allows you to leverage your inventory, equipment, real estate and accounts receivable to secure funding. For larger companies that have strong credit ratings and valuable assets, ABL can help you grow your working capital faster than many other funding products. How? It’s based on a percentage of your assets — so with more assets comes more opportunity. ABL could even offer funding as high as $10 million.

ABL Advantage 2: Discrete and flexible

ABL is also cost-effective, very flexible and discrete – something that most large companies value. You don’t have to change the invoicing process with your customers, and you can almost immediately access a significant amount of working capital.

ABL Advantage 3: Turn inventory into profit quicker

How does this impact the cash cycle? By securing ABL funding, a company will effectively reduce their DSO (Days Sales Outstanding) and reduce the number of days it takes to turn their inventory into cash. The company no longer has to wait the full time to collect on their sales, since the ABL delivers that capital much faster.

Example Scenario: How ABL can work for companies in real life

Clarence is the CFO of a tool manufacturing enterprise that has a large operating facility including a warehouse, office building and manufacturing plant. He prides himself on their impeccable financial reporting and averages 60 days for their accounts payable, and 90 days for collections.

The Sales team is working on a huge deal to sell existing inventory in their warehouse and expects to close that within 45 days. Another big deal is on the horizon that will require the production to ramp up, but cash flow is tight and Clarence needs to find capital to buy all the additional supplies that will be needed.

So he works with Liquid Capital to leverage their manufacturing equipment along with their existing receivables to secure a financing agreement. Liquid Capital approves the deal and advances them the required $2 million in funding 25 days later, taking over their existing receivables. The new deal goes through and Clarence approves the purchase of the required supplies.

| CCC BEFORE ABL FUNDING | CCC AFTER ABL FUNDING |

| CCC = DIO – DPO + DSO | CCC = DIO – DPO + DSO |

| CCC = 45 – 60 + 90 | CCC = 45 – 60 + 25 |

| CCC = 75 days | CCC = 10 days |

Improved CCC by 65 days

What is the end results?

Using Asset-Based Lending, Clarence’s cash flow cycle has dramatically shifted, from 75 days to just 10 days. By freeing up resources, he’s now certain their new deal can go through.

In this example, Clarence was able to access such significant capital by leveraging the company assets in combination with his accounts receivable. For companies in similar situations, it’s worthwhile learning about your options and comparing them against other financing alternatives. By making the most of your options, you could access up to $10 million from Asset-Based Lending with Liquid Capital.

Up Next:

Read Part 1: How to determine your company’s “cash conversion cycle”

Read Part 2: 7 proven cash flow tactics every CFO needs to know

Read Part 4: Learn how to keep suppliers happy and cash in your pocket

About Liquid Capital

At Liquid Capital, we understand what it takes for small, medium, and emerging mid-market businesses to succeed – because we’re business people ourselves. Our company is built on a network of locally owned and operated Principal Offices, so whenever you’re talking to Liquid Capital you’re talking directly to your funding source and a fellow business person.