How to get start-up financing without a bank loan

Start-ups grow fast, and they need to piece together an elaborate puzzle to see the fruits of their labour. That includes brilliant people, endless hard-worked hours and sufficient cashflow. No wonder start-up financing is such an important piece of the puzzle.

It’s incredible to see a young start-up reach new levels in their business, but if the proper financing is missing, they’ll never realize the picture they envisioned. For many, the biggest challenge is getting the working capital to operate at the right scale.

A widely quoted U.S. bank study explained that 79 percent of young businesses failed due to “starting out with too little money.” Bank loans can be extremely challenging to secure at an early stage, and other financing like angel investments can bring its own set of challenges.

Co-founders and young CFOs then spend countless meetings drumming up new rounds of funding, and for good reason. Securing these series of VC funding can mean an incredibly rapid enhancement in growth, but at a cost. With pressure to grow exponentially (sometimes 10x each round) eventually, deals can be made with the wrong partners. Unfortunately, many founders never secure their funding and are forced to abandon their current business goals.

Growing like a weed, but stuck without options

Start-ups aren’t handcuffed to the traditional entrepreneur financing resources. Alternative solutions exist that can be an immediate source of consistent working capital.

For Ted Hope, President of PM Retail Solutions in Scarborough, Canada, that’s exactly what he did when faced with a financing dilemma.

“As a start-up company, you don’t have the credit or history of a more established organization. At the same time, you’re subjected to a lot of COD and cash flow issues,” Hope explained.

Hope was four months into his new business venture, a custom manufacturer of retail store display fixtures, and the outlook for the business itself was looking very promising. In fact, the company brought in almost half a million in revenue in the first six months, but that was exactly the problem.

“We were self-financing, but as we got more sales, I had about $150,000 in A/R that I wasn’t going to see for at least 60 days,” Hope explained. Since they had to wait for customers to pay their invoices, cash flow was tight.

Different kind of start-up financing

For start-ups and growing small businesses, this situation is likely familiar. It’s unfortunate, but 82 percent of businesses that fail, do so because of cash flow problems.

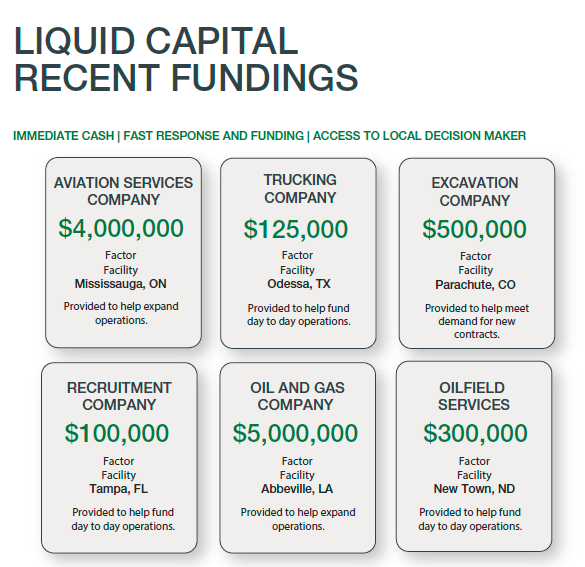

For companies with regular invoices like PM Retail Solutions, they found an alternative solution with accounts receivable financing (also known as factoring). By leveraging those unpaid customer invoices, they could get almost immediate cash flow from their Liquid Capital partner. Hope worked with Liquid Capital to get paid upfront for a significant value of the customer invoices.

The fix was almost instantaneous. PM Retail attained a pre-approval and received $60,000 in their account within only one day of initializing the transaction. Liquid Capital was then responsible for collecting on the customer invoices, and distributing the additional revenue to PM Retail at that time. This also freed up a lot of time for Hope and his team.

Hope had found his solution. “Factoring allowed us to free up our cash flow during a precarious time as a start-up, making us almost instantly capital self-sufficient. We can pay COD for almost everything we do, and have better terms because we have money in the bank.”

Finding the best solution for your start-up

Of course, this solution is one of many, but it’s worth investigating to see if it’s the right one for your business.

Alternative financing specialists can offer you sound advice, and should be able to work as a supplement to your traditional banking options as necessary. In many cases, Liquid Capital will work with clients on both short and long-term timeframes as needed, and can help a client graduate to access traditional bank loans as well.

Until that point, alternative solutions like accounts receivable financing can not only bridge the start-up funding gap, but can be the flexible solution that a founder and CFO have been searching to find.

Every small-business owner is looking for an edge to set their company apart or give them better odds of success. Smaller companies are generally nimble enough to change or adopt new strategies when needed. But these businesses also run on a tight budget, and the trends they focus on need to both be cost-effective and demonstrate quick and tangible results. If the strategies are easy to implement, so much the better.

Every small-business owner is looking for an edge to set their company apart or give them better odds of success. Smaller companies are generally nimble enough to change or adopt new strategies when needed. But these businesses also run on a tight budget, and the trends they focus on need to both be cost-effective and demonstrate quick and tangible results. If the strategies are easy to implement, so much the better.