Set and achieve your business growth goals

Whether you or your client are preparing to win that next contract, hiring more staff or expanding into international markets, set and achieve your business growth goals with these top tips.

With the new year fast approaching, many entrepreneurs are not only setting personal targets but may also have new growth goals for their businesses.

A recent survey showed that 88% of Canadian small- and medium-sized businesses are confident they will grow over the next three years — up from 83% in 2022 — as many adjusted their business strategies in the last 12 months due to recession concerns.

In the U.S., two-thirds of small businesses reported that they were in good overall health in Q3—next year, 71% expect revenue to grow and 40% plan to increase investments and staff.

Setting dynamic business goals starts with a roadmap. Keeping targets achievable, trackable and flexible is key, especially when many businesses report that economic activity and sales growth have moderated this year.

Here are some tips to consider when you and your team are deciding on growth priorities:

Be realistic and clear

Setting growth goals with a good chance of success starts with relevance. Whatever your plans, they must make sense for your business size, sector and current market conditions. This also includes making sure the parameters of your goals are well-defined. and achievable on your timeline.

Did you know? Goals set according to a SMART strategy — Specific, Measurable, Achievable, Realistic and Timely — have a greater chance of being met, says the Corporate Finance Institute.

Be in the know

In line with setting a realistic growth goal is identifying the key performance indicators (KPIs) that will help you track your progress, celebrate wins or course-correct, if necessary. Depending on your business growth goal, this could be anything from financial metrics, such as your working capital ratio or your net profit margin, to HR KPIs, like your employee turnover rate.

Stay flexible

In an uncertain economic environment with a potential recession looming, being able to pivot when necessary may be key to making even incremental progress toward your targets. While your core goal remains the same, staying on track involves planning for various scenarios and their impacts on your goal.

Pivot easily with new tools

Establishing a process for reaching your goals is key — but when it comes to putting your plan into action, you can also evaluate whether there are new tools you can use to achieve or even exceed your growth objectives.

Leverage AI and automation

Consider if your business growth plans would benefit from an investment in artificial intelligence, automation or other new technologies. More than haf of Canadian businesses say AI and machine learning is the most important technology for achieving their short-term goals, followed by robotics and edge computing.

At the same time, says KPMG, tech investments can’t just be made “because others are doing it”—its use must be strategic and clearly related to solving specific business challenges.

Consider ways to innovate

Innovation can help companies grow — but it can also help them adapt to business conditions and stay ahead of the competition. This doesn’t just apply to disruptive innovation reaching into new markets, but also to transformations that enhance your existing offering.

This may be a good opportunity to think outside the box — is your market ready for a new product, a spin on an existing product or service or improvements to what you already offer? Introducing something new or an enriched version of your existing offering can be a growth driver, especially in a challenging economic climate.

Mitigate financial risks

Ensuring you have enough cash flow to fund your growth plans is crucial. But in a rising interest rate environment, companies are facing a higher cost of borrowing. And with tighter lending criteria in place, newer businesses may also have difficulty qualifying for a loan from a traditional financial institution.

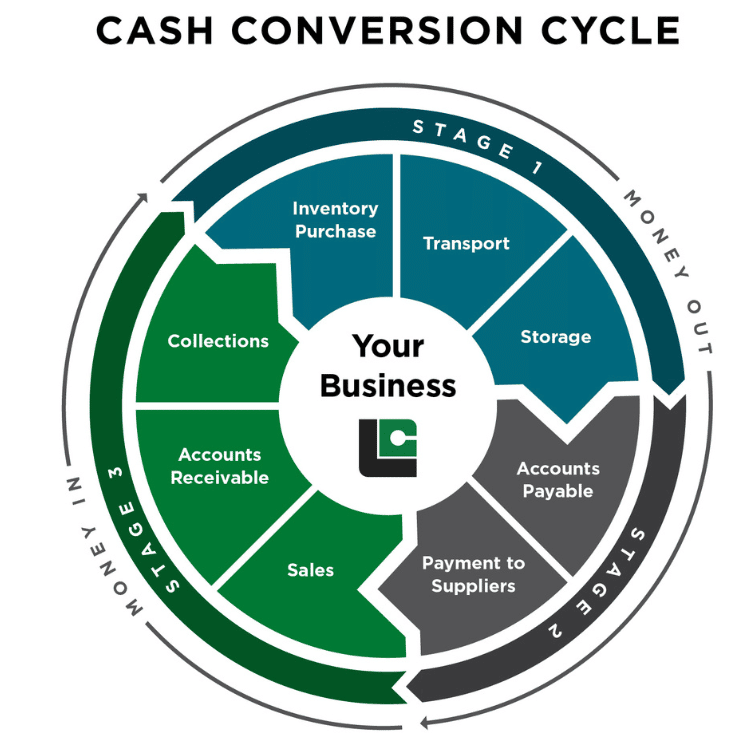

Having a funding solution like invoice factoring on hand can be a useful part of your cash flow management toolkit. Invoice factoring allows businesses to quickly secure a reliable source of working capital by turning near current assets — your credit-worthy invoices — into cash. It isn’t a loan, but rather an advance on payments that are already owed to your business.

With no long-term contract in place, there is also flexibility with this approach. If you have periods where you have adequate cash flow and don’t need to factor your invoices, you can opt-out of the process.

With a clear, agile strategy and a few new ways to achieve your targets, realizing your funding your growth goals is within reach.

Interested in discussing ways alternative funding can help you (or your client) achieve new business goals? Contact a Liquid Capital Principal today.

Evaluate your cash flow situation monthly

Evaluate your cash flow situation monthly