PO Financing can ensure your suppliers deliver — and improve your cash flow!

Part 4 in the Cash Cycle series: Get the inventory you need faster with PO Financing.

For business owners, nothing quite beats the thrill of securing a new — and big — order. Ring that sales bell! But your excitement can extinguish the moment your realize there isn’t enough supplies or inventory on hand to deliver (even if you’re ready to start production.) You may jump to place a rush order with your supplier, but what if they need you to pay in advance or at the point of shipment?

Many companies don’t have the working capital to pay up front. And some can’t get a letter of credit so they can start the order. Will your supplier ship your goods?

If you’re getting more orders than your available working capital can support, then PO Financing could help you cover the cost of product in transit.

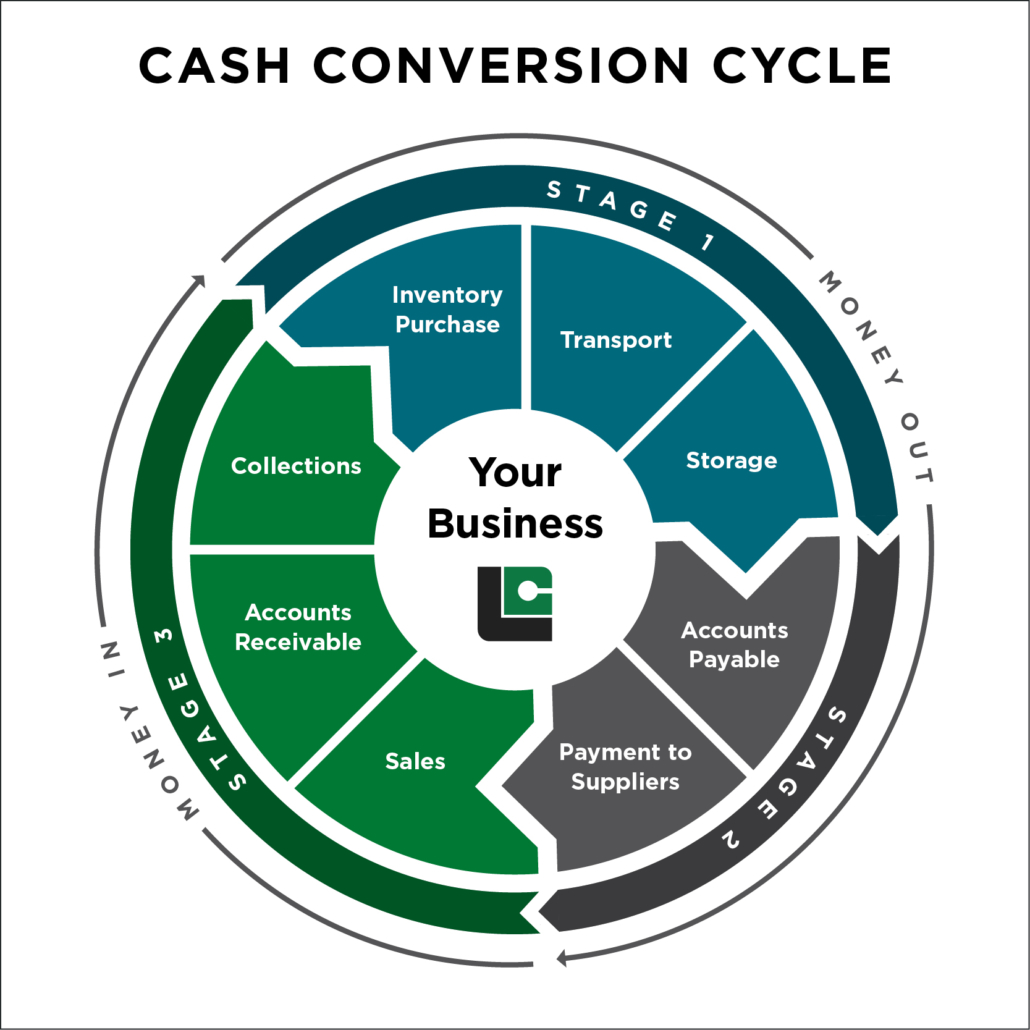

How PO Financing works

Leverage this powerful short-term financing tool designed to help your business grow. Ready to learn about the top three benefits of PO Financing? Keep reading!

PO Financing benefit 1: Increase your available working capital

Purchase Order Financing (PO Financing) helps you close the gap where suppliers are not providing adequate – or any – terms. By extending the number of days you have to pay your accounts payable, you can keep cash in the company and effectively increase your working capital. This financing option will also improve your cash flow, and your cash conversion cycle (CCC), which can help you meet supplier terms.

PO Financing benefit 2: Keep cash flowing through your business

In normal circumstances, you might have to wait 30, 60 or 90 days to collect on your sales (DSO = 30, 60 or 90). But a supplier may demand that you pay immediately before they will release your shipment (DPO = 0). If you don’t have significant working capital on hand, this leaves a serious gap. (More on these figures in a bit.)

As you’re stuck waiting to collect on your invoices, you’re still managing the ongoing costs of running your business and your shipment might not be released. Unfortunately, you’ll never be able to meet supplier terms without finding an alternative solution.

PO Financing benefit 3: Combine with invoice factoring for even more cash flow flexibility

PO Financing can extend your cash cycle and help get your product shipped. When you receive a PO from your customer, you place that with your supplier. As your financing partner, Liquid Capital would then provide your supplier with a letter of credit and they would release the shipment. Your customer invoice is then generated.

With PO Financing, businesses often use invoice factoring to obtain faster payment on their customer invoices once they are generated, so that they can take advantage of both solutions at once.

Example Scenario: Financing the cost of the product

The Gregory twins have been running their online retail venture the past couple years, selling car and truck accessories to the enthusiastic custom car community. Their suppliers are located across North America and overseas, so shipping is a big concern for the duo. Their business is growing, but their cash flow is still struggling. It’s tough to get supplier payments, orders and payments to align.

Currently, their main overseas supplier requires payment at the point of shipment for a large order ready to leave. Once the parts are on the boat, they’re considered sold to the Gregory twins – and time begins ticking – but the duo are cash-strapped and can’t pay the entire invoice. They’re in dire need to get the parts in their customers’ hands, as customer invoices usually take at least 35 days to be paid.

Fortunately, they have major customer orders with supporting POs, and Liquid Capital assists by supplying a letter of credit to the supplier. Liquid Capital finances the Gregory twins’ product costs until the order is delivered to the customer, which takes 12 days to arrive. They’ve secured not only payment but breathing room.

And by factoring their receivables, they’ll now only have to wait 5 days to see cash flow improve from their customer invoices.

| CCC BEFORE PO Financing | CCC AFTER PO Financing |

| CCC = DIO – DPO + DSO | CCC = DIO – DPO + DSO |

| CCC = 60 – 0 + 35 | CCC = 60 – 12 + 5 |

| CCC = 95 days | CCC = 53 days |

Improved cash cycle by 42 days

(Get the full cash cycle formula and descriptions here.)

What is the end result?

With PO financing alone, the Gregory brothers shorten their cash cycle by 12 days. That means they will convert inventory into liquid cash almost two weeks faster.

If they also take advantage of factoring their customer invoices, they could shorten by 30 more days, so their cash cycle is dramatically shortened. That’s a big difference from the three-month timeframe without financial support.

Get more information on the cash cycle, how to calculate it and strategic tactics for your company:

Part 1: How to Determine Your Company’s “Cash Conversion Cycle”

Part 2: 7 proven cash flow tactics every CFO needs to know

Part 3: Leverage your assets to grow your working capital

About Liquid Capital

At Liquid Capital, we understand what it takes for small, medium, and emerging mid-market businesses to succeed – because we’re business people ourselves. Our company is built on a network of locally owned and operated Principal Offices, so whenever you’re talking to Liquid Capital you’re talking directly to your funding source and a fellow business person.