It does not have to end this way

Many small business owners and start-up entrepreneurs get overwhelmed with what they have to do. One of the leading indicators for a failing business is the inability to pay their bills on time. Being overwhelmed, it’s easy to let small things slip and understandable. After all, it’s hard to do everything right when you are just starting out. But some slips can be very costly; taxes and other important payments cannot be neglected, there are severe consequences if you do. Failure to meet payroll is not uncommon for a startup, but those loyal hardworking employees will eventually leave if not paid on time.

The most common reason that a business cannot pay their bills is because their customers don’t pay them quickly. Waiting a long time for a payment from customers is commonplace, but it’s hard to meet payroll and pay for expenses when you are not getting paid for your services and/or goods.

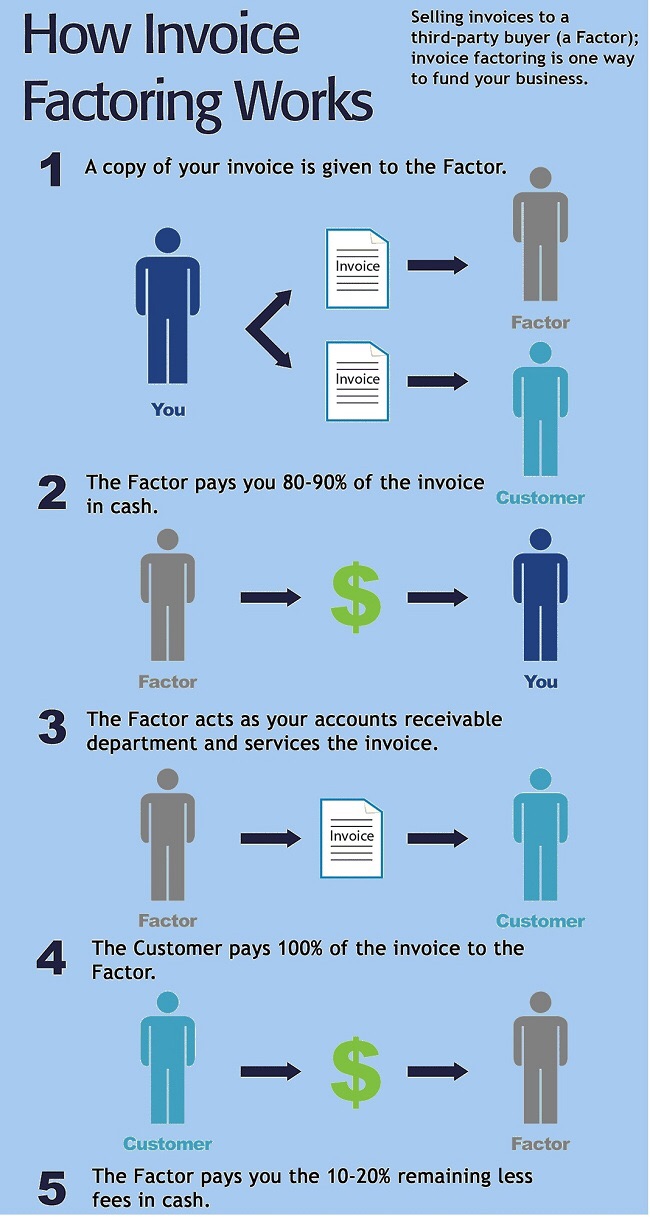

Factoring, or selling accounts receivable to a third-party at a discount, can dramatically raise your capital. It’s not a new practice either; many businesses have used factoring processes to help manage their cash.

It might seem like an expensive endeavor, but when it’s hard for you to manage your money and time, factoring companies can help you to stay on top of your business. Factors will give you 75 to 80 percent of your invoices immediately, and forward the rest of the payment (minus what you’re paying for the service) back to you when your customer pays you.

Think of factoring companies more like extending your credit line (not a loan or liability). Factoring is an asset that allows you to be more concerned with your clients and your service, rather than worrying about your customer’s ability to pay and timeliness of payments. The factors fees are usually pretty nominal (between 2 and 3 percent), but the services they provide are worth much more than that. Additionally, there’s a lot of misconceptions that factoring is a last ditch effort, but it’s not. Usually, factoring is for businesses that have a lot on their plate. Factoring provides these businesses the on-hand cash that they need to grow.

There are 5 big reasons that factoring services aren’t expensive for businesses (they’re actually hugely beneficial):

- Factoring can raise money for your business, fast

Factoring deals often happen in less than 24 hours, and this quick turnaround can give your business critical capital that expands operations immediately. The other alternatives are to apply for loans or wait to hear back from your customers- and neither usually happens very quickly. Small businesses don’t have weeks to wait or months to wait for income, businesses need immediate action.

- Businesses that factor can bring in money without filing for loans

Debts can be useful to build businesses, but it can be extremely risky. This is because businesses badly need capital in many phases of development. If you don’t take action for your business now, you’re going to have to have a loan. The more immediate the loan, the more expensive it will be. Factor costs are fixed, and take care of a very important aspect of your company- the cash flow that makes your company grow.

- If your business can’t get a loan, factoring could be a great alternative

It’s never been easy to get business loans, but now it’s even more difficult because so many businesses fail. Banks ask for higher and higher rates and refuse to give money to businesses that do not have an extensive credit history. If your business hasn’t been around long, has had problems making payments, or doesn’t have a lot of spare capital it’s unlikely that your business can get the loan that you need. In these circumstances, factoring services are some of the only options for businesses.

- Often, businesses have collection departments that are non-existent or understaffed, but a factoring company’s isn’t.

Does your business have several employees dedicated to paying the bills, filing invoices, and contacting clients? If you do, you don’t need them anymore because factoring provides one of the cheapest, most efficient services out there. Not only do factors provide your business with money in 24 hours; they also keep track of your invoices and tardy customers, because they’re getting paid for it (it’s built into their fee). So not taking advantage of it is poor business practice. Paying a factor is cheaper than keeping your credit and collection employees. The factors have a professional staff trained in collecting invoices; you don’t have to worry about that anymore.

- Factoring is inexpensive!

The «high costs of factoring services» are grossly misunderstood. In reality, most factor services are inexpensive when you compare what it costs to not have that money right away and to have employees dedicated to collecting payment. Plus, factoring services usually get money from clients within 30 days. This means that when businesses factor, the cost of the service is usually about 2 or 3 percent for nearly a month of financing for amounts up to 75-80 percent (and the money is received right away).

Whenever you assume that factoring services are too expensive, you should also yourself a few questions:

– Could you get needed capital (such as a bank loan?) the next day?

– How much would it cost, even for a small loan?

– Is your understanding of the costs of financing accurate? Have you considered the benefits of factoring?

More often than not, you’ll be pleasantly surprised with the results that you find when you consider the benefits of factoring. Factors free your business from worrying about having the money to grow your business.