Bullet Points: How Asset-Based Lending Increases Cash Flow

Time is money, and when you’re in need of cash flow you need to get information fast. Let’s cut to the chase with the bullet points on asset-based lending.

What is Asset-Based Lending (ABL)?

- An asset-based loan allows you to leverage your accounts receivable, inventory, equipment and real estate in order to get access to working capital

- It can be a loan from 6 – 24 months, but generally averages around 1 year

- Often used by established companies with definable and identifiable internal processes and controls.

What assets can be used for ABL?

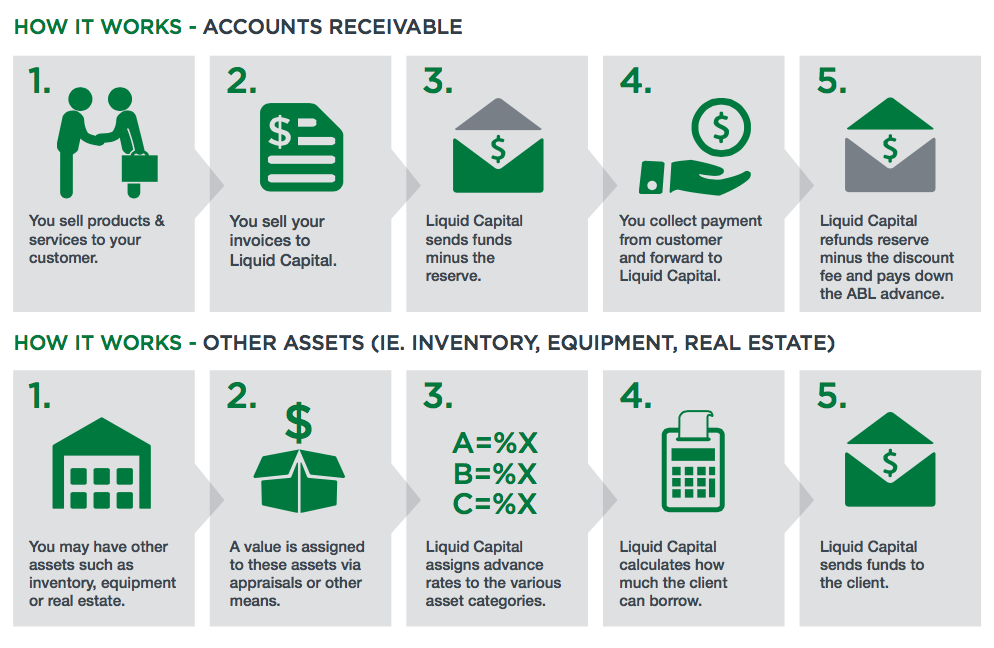

- Accounts receivable: Invoices that customers owe you now or in the future

- Inventory: raw materials, work in progress or finished goods sitting in your warehouse

- Machinery and equipment: Funding can be up to 75% of the liquidation value.

- Real estate: Register a collateral mortgage against residential or commercial properties. You may also check into your property values with an up-to-date appraisal from your real estate agent. Liquid Capital can provide more info on the process.

Why would your company turn to ABL?

- It’s a more flexible type of financing

- Well suited to companies with seasonal sales

- If you’re in rapid growth stages, it can get you faster access to cash flow

- Clients outside of covenant with their bank may find this is a better option

To qualify for ABL, your company should:

- Have a strong credit rating

- Have comprehensive financial reporting and internal controls

- Monthly financial statements

- Aged A/R and A/P summaries

- Have proven success and a good track record

Read Related: What is accounts receivable financing and factoring? Leverage unpaid invoices and turn them into liquid cash flow.

ABL may be right for your company if you are:

- Short on working capital

- Fall shy of bank loan criteria

- Have seasonal capital requirements that don’t fit into the bank loan structure

- Looking for lower rates than a factoring solution

- Not looking for a long-term contract for financing

- Consider optics important and you don’t want your client experience to change. Discretion is key with non-notification ABL, typically available to larger businesses. Check with your Liquid Capital Principal to see if this is available to your business.

- Payments are deposited into a “sweep account” (typically at your bank) and your client is never aware that Liquid Capital is handling your financial transactions.

- In a strong growth cycle and need quicker access to working capital.

- Liquid Capital calculates borrowing amounts on a weekly basis, compared to banks that traditionally do this on a monthly basis. If you’re growing, your ability to borrow will increase.